Abstract

Nicholas Mulder examines how, despite strong fundamentals, the Dutch economy has suffered due to high levels of household debt.

By Nicholas Mulder, Columbia University

In 1977, The Economist coined the term ‘Dutch disease’ to describe what was then taking place in the economy of the Netherlands. Since the discovery of a large natural gas field in 1959, the guilder started to strengthen in international markets as exports boomed. Though good for state coffers, this currency appreciation made Dutch manufacturers much less competitive. Industrial productivity fell and unemployment rose. In the wake of the oil shock, The Economist warned, using gas revenues to fund lavish socialist welfare policies was a recipe for industrial decline. The journalistic standard-bearer of economic liberalism recommended fiscal rectitude and competitiveness as the keys to export-based growth. From that point on, ‘Dutch disease’ became an oft-diagnosed condition of commodity-exporting economies (especially oil and gas producers) from Nigeria to Indonesia and from Chile to Russia.

Four decades later, no one any longer associates Dutch disease with the country that lent its name to the phenomenon. The Netherlands has rebounded from its late industrial troubles. As a globally competitive export powerhouse, its current account has been positive without interruption since 1981; on average, the annual current account surplus was 3 percent in the 1990s, 6 percent in the 2000s, and since 2010 has reached an astonishing 8-11 percent.[i] The World Economic Forum lists the Netherlands as the fifth most competitive economy in the world.[ii] Not even Exportweltmeister Germany has a balance-of-payments position as strong as the country headquartering multinationals like Royal Dutch Shell, Philips, Unilever, Heineken, DSM, AkzoNobel and Ahold. The Dutch corporate sector reinvests these export earnings by exporting capital to the rest of the world. Forced retirement schemes have plowed further savings into investment abroad. As a result, Dutch pension funds are proportionally the largest in the world, with over 1 trillion euros of assets—some 144% of GDP in 2012.[iii] It seems that the Dutch are high and dry.

But the Great Recession has unearthed a number of problems that undermine this impression of stability, sustainability and success. In the wake of the financial crisis, the Dutch economy experienced a double-dip recession as GDP contracted in 2009 (-3.3%), 2012 (-1.6%) and 2013 (-0.7%). Currently, the IMF forecasts just 1.8 percent growth for 2016. For all its supposed long-term strength, in the last decade the Netherlands has been unable to translate its booming export surplus into broad-based growth. Household income and investment have not recovered from the crisis. Wealth inequality has surged.

This article examines what is at the core of these problems: the accumulation of an enormous amount of debt by Dutch households and banks in the decade and a half before the financial crisis. A global credit boom was amplified locally by the Netherlands’ strong integration in Euro-American corporate and financial networks, and due to specific institutional and legal characteristics of the Dutch economy. Chief among these a unique provision that makes interest paid on mortgages tax-deductible. Homeowners were hereby incentivized to take on very high leverage and discouraged from reducing their mortgage debt. Nine years after the crisis, forty percent of the population of one of the richest countries in the world has negative net wealth.

In order to understand how the problem of private debt in the Netherlands developed from the late 1980s onward, I first provide an overview of the housing market. I then situate the housing market and mortgage in the context of the very large Dutch financial sector and the emergence of a broader northern European ‘overbanking’ problem. I also draw attention to how the collapse of this bubble and subsequent deleveraging has affected income and wealth inequality. Finally, I elaborate what this means for future growth prospects. Only macro-prudential improvements combined with fiscal and industrial policy aimed at increasing labor income and investment can correct inter-sectoral imbalances while preventing renewed debt buildup. The Dutch situation is instructive for the twenty-first century. This is not because it is the next big bubble in the world economy. Rather, the Dutch case demonstrates that net robustness does not solve gross problems. In spite of strong exports and net international investment positions, the Netherlands faces the problem of charting a balanced growth path in a world of high private debt.

*

The Netherlands has been an international hub of financial capitalism since the 17th century when the country was the pre-eminent trading nation of the world and Amsterdam its global financial center. After stagnating in the eighteenth century and industrializing relatively late in the nineteenth century, the Netherlands started to regain its position in international markets in the interwar period, to some degree thanks to commodity exports from the Dutch East Indies. After 1945 it followed its larger neighbor and main trading partner Germany in developing a strong export position in manufacturing and agriculture. High growth and export earnings allowed the erection of a substantial welfare state, high-quality public infrastructure, and a generous pension system. The country became famous for its corporatist system of managing labor relations—the so-called poldermodel—in which employers and unions negotiated a guided wage policy.

The stagflation of the 1970s threatened to undermine this economic consensus. In 1982, employers’ organizations and labor unions negotiated the so-called Wassenaar Agreement, in which workers accepted wage restraint in return for shorter working hours. This enabled the Dutch government to maintain its commitment to low inflation and a strong guilder, which was one of the few currencies to successfully track the German mark during the 1980s. Having taken a leading role in pushing forward European integration and the completion of the single market, this set the stage for intensified growth in the subsequent decade.

Household debt and the Dutch housing market

In the late 1980s, credit expansion started to play a larger role in the growth of the Dutch economy. With welfare trimmed and wages restrained, financialization offered a means for the Dutch population to boost its standard of living and level of consumption. Due to high taxes and forced pension contributions, households were happy to gain access to easy credit.

Figure 1. Private credit growth in the Netherlands 1961 – 2013[iv]

In this context, one of the peculiar features of the Dutch fiscal system became very salient: the mortgage interest deduction (hypotheekrenteaftrek), which had been first introduced in 1914. Under this deduction, interest paid on one’s mortgage can be subtracted from one’s taxable income. This means that households can lower their taxable income with large mortgages, for the larger the mortgage loan, the more interest has to be paid on it annually. This measure benefited, in particular, those households with high-valued properties acquired through leverage. From the 1990s onward—simultaneous with similar measures, such as Bill Clinton’s National Home Ownership Strategy in the United States—the mortgage interest deduction was promoted as an official incentive to create a population of homeowners. The mortgage interest deduction became widely and many middle and lower-income households also profited from it. In 1990, Dutch households paid a total of 3% of GDP (7 billion euros) in mortgage interest; this figure rose to 5.4% of GDP (33 billion euros) by 2009.[v] The provision was not only a major subsidy to household debt with macroeconomic effects. It also weighed seriously on public finances: by 2014, the effective tax break provided by mortgage interest deduction was equal to 14 billion euros a year—some 2 percent of Dutch GDP.

Similar measures did and do exist in other countries such as Belgium, Sweden, Switzerland, the United States and the United Kingdom. But most have been restricted in their effects, phased out or are trivial in their macroeconomic effect. In Belgium, mortgage interest deduction has existed for a long time, but since 2005 the tax-deductible amount of interest has been limited to 3120 euros a year. In Britain, the measure was phased out from 1979 onwards and disappeared completely by 2000. Sweden also operates a deductibility provision, but its size was limited to 21-30% of the interest in 1991 amidst an incipient recession (the phase-out itself may even have burst the housing bubble that the deduction had created). Switzerland has full deductibility, but its mortgage lenders and banks never extend loans worth more than 80 percent of a property’s value. This way, homeowners have a 20 percent equity buffer in case the market takes a downward turn. Finally, the IRS allows homeowners to deduct mortgage interest expenses on property up to $1 million from their tax bill. But due to the low overall level of taxation in the United States, the advantage obtained by homeowners—and the disadvantage that is borne by the government—is much smaller.

The Netherlands was, therefore, the only country prior to the crisis that had both unlimited deductibility provisions and very generous lenders willing to provide interest-only loans with up to 120% loan-to-value ratios. Mortgage interest deduction had a very large effect on the economy and on private debt growth precisely because of the high level of income taxation in the Netherlands. Thus it is not true that private debt growth in advanced economies during the Great Moderation was a substitute for a redistributive welfare state that had broken down or been dismantled in the 1980s. Dutch income taxes and social provisions continued to be high.[vi] Rather, household leverage was an escape of sorts from a system that imposed tax- and pension-related burdens on all. Due to the existence of its peculiar tax break on mortgage interest, the country’s very progressive fiscal system, in fact, encouraged large private debt growth.

The provision was politically unassailable—any attempt to discuss its reform was seen as a destabilizing move in a country with fragile coalition governments. In a 2006 poll, only 18% of the population was prepared to abolish the deduction. Throughout the extraordinary trans-Atlantic credit bubble that started in the 1990s and grew at breakneck speed in the 2000s, total credit to households mushroomed to 119% of GDP in 2010; only Denmark was more profligate in extending loans to households (credit to households there rose to 136% of GDP). These two small northwest European countries were exceptional in the size of the household debt that they built up.[vii] Meanwhile, the housing market across the country was booming. Property prices soared across the country; on average they almost trebled in thirteen years, rising to 291% of their 1995 level by the third quarter of 2008.

Figure 2. The Dutch real estate boom, 1995-2016

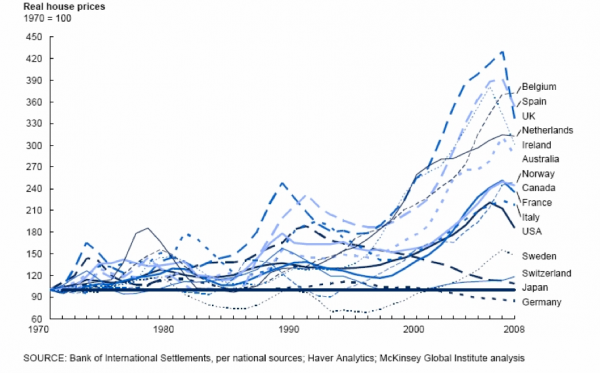

In comparative perspective, this boom was among the largest ones in the last five decades. Measured from a 1970 baseline, only the UK, Ireland, Belgium and Spain had more inflated real estate markets. In 2008, the IMF’s World Economic Outlook warned that house price overvaluation in the Netherlands was the second-highest among advanced economies and that this inflation was due for a serious correction. It noted that ‘mortgage interest deductibility fuels these increases, reduces affordability, and discourages amortizing loans, exacerbating households’ vulnerability to price swings and interest rate shocks. Therefore, the mission reiterates past advice to limit mortgage interest deductibility, removing rent controls, and easing zoning restrictions to stimulate housing supply’. [viii]

Figure 3. Real estate bubbles across the OECD economies compared, 1970-2008[ix]

When the bubble burst, the collapse of the housing market was severe: from 2008 to 2012 it fell more than a quarter. As a result of the large mortgage debts held by the Dutch population, many households saw their net wealth enter negative territory as their outstanding mortgages were now worth more than the reduced value of their property. Unlike in the United States, under Dutch law there is no way of canceling mortgage debt by returning home ownership to the mortgage provider or bank in question; if the sale value of property is less than the mortgage value, any residual remains payable even after an indebted homeowner manages to sell his property. As real estate prices kept falling, the number of underwater mortgages thus shot up, nearly trebling in the six years after the peak of the housing bubble. By 2014 some 1.48 million households—35 percent of the Dutch population—reported that their property value was lower than their mortgage debt.[x] At the moment, Dutch home prices are still 14.6 percent below their August 2008 peak. The number of underwater mortgages is shrinking slowly but remains large.

The severity of this situation prompted some political reforms of the mortgage interest deduction. It became increasingly difficult to justify leaving the deduction fully intact, especially when budget cuts elsewhere made the tax break that it provided stand out in its size relative to other state expenditures. In 2013, new legislation made interest paid on mortgages tax-deductible only for mortgages that are amortized over a thirty-year period. Interest-only loans are therefore a thing of the past. In addition, the loan-to-value ratio of the provision is being brought down to 100 percent by 2018—it is currently at 104%. In the long run, the total deductible interest will be brought down by a few basis points a year until it reaches 38% in 2040. By that time, it is hoped, other macro-prudential measures will have prevented another housing bubble.

The Dutch financial sector: debt securitization and leverage

The high household mortgage debt in the Netherlands does not exist in a vacuum. It is related to the systemic buildup of debt in and by the Dutch financial sector. With total assets more than 3 times the size of the Dutch economy, the financial sector is large by international standards of comparison—the only countries with proportionally larger financial sectors are Switzerland, Luxembourg, Malta, Cyprus and several Caribbean offshore centers. No top-20 global economy has a financial sector of this scale.

Figure 4. National financial sectors of 15 OECD economies: leverage and relative size

BIS consolidated banking statistics show two remarkable things about the Dutch financial sector. First, it is among the most highly leveraged in the world. The Dutch financial system has an equity-to-asset ratio of only 5.5 percent. In other words, it is leveraged 18 to 1. Compare this with the leverage ratios of the US (9 to 1), Turkey and Greece (9.5 to 1), Italy (14 to 1), the UK (15 to 1), Australia (15.6 to 1) France and Belgium (17 to 1), Sweden, Switzerland and Canada (17.5 to 1). Among all advanced economies, only Finland is more leveraged at a ratio of 21 to 1.[xi]

In addition, the balance sheet of the Dutch financial sector is extraordinarily dependent on debt for funding. At the end of 2015, the Dutch financial sector had total assets of $2.554 trillion dollars; of its liabilities, some $719bn (29.7 percent) were debt securities. By contrast, the US financial system has total assets of $13.6 trillion dollars, but only 4.2 percent of its liabilities are made up of debt securities, much less than the Dutch financial system. The UK financial sector balance sheet is 7.8 percent debt-funded; that of Switzerland, 15 percent. In terms of the total stock of debt securities, only the French and German financial sectors outranked the Dutch, but overall these banking systems remain less dependent on debt, which constitutes just 13.6 percent of their liabilities. Dutch banks and other financial institutions (pension funds, money market funds, etc.) have issued a whopping 11 percent of all the international debt securities that are currently outstanding.[xii] Finally, the Dutch financial sector also highly concentrated—the five largest credit institutions hold over 80 percent of all assets in the financial system.[xiii] Within Europe, only Estonia has a more concentrated financial system.

It is the fragile combination of large size relative to GDP, high leverage, debt finance dependence and institutional concentration that makes the Dutch financial sector an unstable outlier in the world economy. The problem becomes even bigger when one includes shadow banks. Within Europe, these are predominantly concentrated in Ireland, Luxembourg, and the Netherlands.[xiv] Money market funds and special financial institutions (SFIs) belonging to multinational corporations hold around 3.3 trillion euros of assets in the Netherlands, larger than the entire official banking sector captured in the BIS statistics combined. Add in the 1 trillion euros of assets controlled by Dutch pension funds (the largest in the world) and one starts to get an adequate impression of the size of financial shadow balance sheet of a $752bn economy with 17 million inhabitants.

Inequality and the shock to incomes

The dramatic financial development of the Netherlands since the early 1990s exposes a dimension that clashes with the country’s international reputation (and its own self-image) as strongly egalitarian. Studies of inequality in the Netherlands in recent years show a remarkable divergence. What is striking is the enormous gap between income inequality (which is lower than the OECD average) and wealth inequality (which is among the highest in the OECD). This combination of a relatively egalitarian income distribution and an extremely unequal wealth distribution is a mark of the economic development that we have described above: a household sector that heavily indebted itself due to leveraged home values, only partially compensated by a redistributive welfare state erected on top of a productive services and manufacturing sector. The debt buildup preceding the crisis and the subsequent debt overhang have achieved something fairly unique among advanced economies—a disjuncture between income and wealth inequality, which in most countries are quite closely related.

The top decile of the wealth distribution possesses almost 60 percent of the net wealth in the Netherlands; the top percentile owns 24 percent of total wealth.[xv] By contrast, the bottom 40 percent of the wealth distribution has none or negative net wealth. This corresponds almost exactly with the 35 percent of the population whose home values are lower or equal to their considerable mortgage debt. Data from the Dutch central statistical bureau show that the gap between income and wealth inequality is large and widened during the crisis. In 2006, the Gini coefficient of income inequality was 0.27, on the low end of the OECD spectrum between 0.24 in Denmark and 0.38 in the United States. In the same year, the Gini coefficient of wealth inequality was around 0.80. With the housing market collapse triggering a large fall in the already thin net wealth of millions of lower and middle-class homeowners, an increasing part of the population fell out of the wealth distribution altogether. As a result, wealth inequality has reached even higher levels. By 2014 the Gini coefficient had risen to 0.89.

As one might expect, the Netherlands scores high on virtually all international metrics of private indebtedness. According to OECD data, in 2014 the Netherlands had the second-highest household debt among all industrial economies. The average Dutch household debt stock was 277 percent of net disposable income (only Denmark had higher indebtedness, at 308 percent of net disposable income). This is especially high when compared to other countries that are considered to have experienced serious mortgage debt-driven financial crises in 2007-2010, such as the United States (113 percent), Spain (127 percent) and the United Kingdom (156 percent).[xvi]

The debt burden borne by the Dutch is not just proportionally high but also in terms of the annual flow of income that needs to be devoted to paying down debt—the debt service ratio. Throughout the 2010-2014 period, Dutch households have faced a debt service ratio of 18-19 percent of their annual income, more than twice that of households in the United States and even in Spain and Portugal.[xvii] In those countries the median debt-to-income ratio was between 114 and 134 percent in 2010; but in the Netherlands, it was a whopping 194 percent, an outlier in the OECD crowd. All these descriptive statistics tell the same story: the country is dealing with a very heavy private debt overhang, and its household sector is likely to continue to struggle for years as the export-oriented corporate sector is capturing most of the income growth.

As a result of financialization, Dutch household spending capacity is very dependent on their stocks of financial assets (especially pensions and savings accounts) and liabilities (mortgage debt). All of these are directly influenced by volatility in financial markets. In recent years, low-interest rates due to quantitative easing by the ECB have lowered mortgage burdens but depressed the value of pensions. Unsurprisingly, this exposure to financial volatility means that Dutch consumption behavior is much more erratic than in other countries.[xviii] With little ability to rely on counter-cyclical government spending (most of which went into bank bailouts rather than fiscal stimulus), household finances were doubly affected through loss of income and wealth.

Research by the McKinsey Global Institute from July 2016 indicates that the Netherlands has been particularly strongly affected by the stagnation of household incomes. Across the twenty-five countries studied the weighted average share of households whose disposable income between 2005 and 2014 was flat or falling was 20-25 percent.[xix] However, in the Netherlands, some 70 percent of households experienced stagnant or declining disposable income. The only country with a larger standstill or drop in disposable income was in Italy, where every income segment was affected. That serious loss in income growth happened during the crisis and its aftermath is unremarkable. What is striking is that of the two countries whose populations were most severely affected, one is now seen as the Eurozone’s next weakest link, while the other is held up as a paragon of economic virtue.

Figure 5. Percentage of households with flat or falling income, 2005-2014[xx]

The differences in how market income and disposable income were affected by the crisis are mainly due to varying macroeconomic responses. In France and the United States, for example, government intervention in 2008-2009 led to a ‘cushioning’ of disposable incomes. In the Netherlands, automatic stabilizers and transfers did not actively worsen the stagnation and fall of incomes (as it did in Italy). But the Dutch government has done nothing to improve the deterioration of disposable income either. Given that on average most advanced economies managed to reduce the degree to which market income decline affect disposable income for at least two-thirds of the affected income segments, this must be counted as a serious failure to protect household income and maintain macroeconomic demand.

The challenge of deleveraging

The psychological effect of this income loss on both household spending and corporate investment has been considerable. When we look at how consumption and investment have fared under the debt overhang, the continued weight of household debt is clear. Household consumption has fallen from a pre-crisis peak of 46.3 percent of GDP in 2006 and seems to have been permanently depressed by 1.5-2 percent—it was 44.6 percent of GDP last year. Investment took an even larger hit during the Great Recession. Gross fixed asset formation, which was at 23 percent of GDP in 2008, constituted only 19 percent of GDP in 2015. In absolute terms, it is still 8 percent below its erstwhile nadir.[xxi]

The Netherlands is an unusually open economy: exports and imports together are larger than GDP, due to the high amount of re-exported goods. Long-lasting declines in household consumption and investment mean that the country’s natural reliance on external demand will intensify. With two out of the three core components of the domestic economy weakened, only government spending and foreign demand are able to deliver overall economic growth. This explains the structural rise in the current account surplus to around 10 percent of GDP in the last few years. As beneficial as this may seem from a balance of payments perspective, it is a resilience-reducing development. With deleveraging households less able to put a floor in effective demand, the vagaries of the global trade cycle in an uncertain world economy will have an even larger effect on Dutch GDP.

Low inflation has done much to weaken the Dutch recovery. It has been below the ECB target and falling for several years. It averaged only 1 percent in 2014 and slipped down to 0.6 percent in 2015; in the first quarter of this year, inflation remained at 0.6, before falling to zero in the second quarter of 2016.[xxii] In other words, the country is in danger of tipping into deflation. The low inflation is a result of the reduced household spending. But although it preserves the value of stagnant nominal incomes, it also maintains the real value of household debt burdens as they seek to deleverage.

As the EU Commission has observed, the legal and fiscal obstacles to private investment are minimal in the Netherlands. There is no good institutional reason for this lagging recovery other than the climate created by years of budget cuts that make businesses uncertain about the growth potential of many domestic locales. However, the uncertain domestic investment environment cannot be seen as separate from government policy and regulation, which has tended to be fiscally very conservative in the last decade. Dutch support for the Fiscal Compact is driven by a domestic political consensus to reduce public debt.

In spite of this focus on fiscal prudence, the operation of automatic stabilizers and the second dip of the recession in 2012-2013—which was entirely due to fiscal consolidation in the Eurozone spearheaded by the Netherlands and Germany—caused government debt to rise from 42 percent of GDP in 2007 to 68 percent in 2014. Over the last year and a half, the debt-to-GDP ratio has been falling (it is currently at 65 percent of GDP[xxiii]) due to two reasons. First, rising net exports have increased GDP. Second, the ECB’s quantitative easing has lowered yields on government debt into negative territory, which means that the Dutch government now reduces its overall debt stock when it rolls over short-term debt. However, this reduction of the government’s spending profile brings the continued imbalances in the private sector into starker view.

In this sense, the Dutch predicament mirrors that of Germany, another highly productive export economy with a current account surplus that is facing declining infrastructure spending and domestic investment for entirely self-imposed reasons. A more long-term reason to worry about a low rate of investment is that in its absence, there will be no road left towards future growth but renewed credit expansion. Investment in productive new industries such as renewable energies, biotech, and information technology is not, as it is in many other countries, a pipe-dream for the Netherlands. The country possesses world-class enterprises in these sectors and has a very strong educational system maintaining a highly-skilled labor force. But it can only realize such opportunities if credit and investment from retained earnings are channeled into these ventures through public-private collaboration.

If global trade picks up and deleveraging continues without interruption, the Dutch economy can enjoy a good recovery. But it is equally likely that the size of private debt will remain roughly proportional with GDP even as growth returns. In that case, the debt overhang problem will be there to stay. This is a scenario sketched by Adair Turner in his recent book Between Debt and the Devil: Money, Credit, and Fixing Global Finance (2016). Real estate lending plays a central role in Turner’s argument, and the centrality of private debt and mortgage credit in the Dutch case adds further credence to his analysis.

The Dutch private debt stock grew rapidly to more than twice the size of the gross domestic product in the years leading up to the crisis. Much attention during the European sovereign debt crisis has focused on public debt levels. What is less known as that the EU also has guidelines for what constitutes sustainable private sector debt, which it currently recommends should not exceed 133% of GDP.[xxiv] With total private debt relatively constant at 230-233 percent of GDP since 2009, this means the Netherlands has an enormous imbalance to deal with.[xxv] Dutch household borrowing was proportionally as big at the end of 2015 as it was at the end of 2008 – about 111 percent of GDP. Together with corporate non-financial borrowers, this means that total private sector non-financial borrowing has remained steadfastly at 240-245% of GDP.[xxvi]

A small amount of private debt was taken by the government over through automatic stabilizers, bank bailouts and guarantees, but early fiscal consolidation prevented a large inter-sectoral transfer from occurring. Government austerity policies also induced a second recession in 2012-2013, which further increased the real value of private debt. What has shifted is the sectoral composition of private debt. Whereas during the Eurozone crisis a large and rising part of private debtors were households, in the last three years it has been corporate debt that has grown slightly as households have engaged in a lengthy deleveraging process. However, households and the corporate sector differ in their ability to service debt. Many households suffer from a combination of negative equity, reduced income, and are adversely affected by low inflation. By contrast, the corporate sector has continued to be a large net saver (9-10% of GDP) and has regained its pre-crisis profitability, mainly by seeking export markets outside the depressed Eurozone. Yet because of weakened domestic consumption, corporations have not used retained earnings for investment, but instead spent them on share buybacks and foreign equity investment. This emergent ‘dual economy’ within the private sector itself is cause for concern, not just from a macro-prudential, but also from a political and social point of view.

Future outlook

How might all this be resolved? Because of the inter-sectoral nature of the debt problem, an imaginative fiscal stimulus, an industrial policy aimed at investment, and further improvement of the macro-prudential framework are all steps in the right direction. Many of the welfare state features of the Dutch political economy have serious financial implications. The enormous Dutch pension funds need to be at the center of financial stability policy, for it is their increasing hunt for yield in a world of low-interest rates that will exert pressure towards more risk-taking and higher leverage on the consolidated national balance sheet in the decades to come.

Putting the strength and stability of the household sector back at the center of economic policymaking is perhaps the most fundamental change that needs to take place. In the absence of increased wealth and income redistribution, it is difficult for working and middle-class households to improve their standard of living without leveraging their home equity. This is as likely as in the past to lead to another credit bubble. The Dutch housing market bubble was an intensified local manifestation of the great trans-Atlantic credit boom of 2000-2007. It was caused not so much by the obfuscation of risk in complicated derivatives (although this did affect some Dutch banks that were heavily involved in the American housing market), but through the simple inundation of Dutch society with credit. The slow phasing out of mortgage interest deductibility will delay home price inflation, but the unprecedented external influence of the ECB’s quantitative easing program—which looks likely to be extended well into 2017 since the Brexit referendum has led to lower growth expectation—may well fuel asset price bubbles elsewhere.

The continued low-interest rate policy of the ECB has drawn increasing criticism from Dutch central bankers and policymakers since it lowers the returns on stock portfolios held by pension funds. Given the importance of pensions to the overall capital stock of the Dutch economy, the effects of decreased returns on overall growth are real. But it is not clear what would improve the long-run financial stability of the country. Low rates encourage further risk-taking and investment in unorthodox assets in the hunt for yield. But high-interest rates stifle the economic growth that the pension funds need to deliver stable returns in the long run; moreover, they also skew the economy to a financially top-heavy structure. The recognition that the Netherlands is a finance-intensive economy suggests that its private debt problem may be a twenty-first-century version of the old Dutch disease diagnosed in the 1970s. This time, however, the resource curse at the heart of stagnation is not uncontrolled natural gas exports but uncontrolled mortgage lending.

It is important to be clear about why the situation in the Netherlands is a cause for concern. The Dutch economy is not a basket case on the brink of catastrophe. It is better prepared than many other countries that have been buffeted by deleveraging, austerity and balance of payments crises in recent years. If its political elite and electorate would choose to do so, the Netherlands could easily mobilize the economic resources to resolve many of its problems, from debt overhang to aging. The problem is not one of singularity, but of similarity. What should worry us is how the Netherlands was hit by exactly the same kinds of shocks as the core crisis countries: the US, the UK, Ireland and Spain. The Great Recession managed to inflict serious damage on the Dutch economy and on the financial position of Dutch households in particular. The ensuing problems, economic as well as political, are also found elsewhere in the world: a falling share of wages in national income, rising inequality, and fierce resentment towards globalization, immigrants (in particular of non-European and Muslim backgrounds) and the European Union. A future of economic stagnation will make this political and social instability much worse than it already is.

If even an advanced, surplus-accumulating export powerhouse with a highly skilled labor force was not able to escape private debt accumulation leading to housing market collapse, income collapse and rising inequality, then no economy in the world is not at risk. These problems are global in their reach, and a focus on fiscal virtue and global competitiveness cannot prevent them from affecting all of us. It is time to think different about how to navigate the high-debt future ahead of us.