Abstract

The Troika’s bailout policies have spurred a debt deflation in Greece. Instead of helping the Greek economy, they have replaced public with private debt.

Lara Merling, Center for Economic and Policy Research and The Minskys Blog

Introduction

Greek public debt debacle and the bailout received by the government from the European Central Bank (ECB), the European Commission (EC), and the International Monetary Fund (IMF) – referred to collectively as the “troika” – has been making headlines for years. However, very little attention has been paid to the debt crisis in the Greek private sector. An alarmingly high portion of private sector borrowers is behind on their debt payments, and the Greek banking system currently has one of the highest ratios of delinquent loans in the European Union.[1]

This collapse of debt prepayments is a direct result the policies imposed by the Troika and threatens the future of Greek economic growth. After the Greek government required financial assistance from international creditors, it was forced to introduce draconic austerity measures to repay its debt. Cutbacks to state services collapses in incomes, and an increasingly unstable economic environment contracted spending, therefore, eliminating future cash flows that private entities expected to use to repay their debt. The result has been a spiral of collapsing demand and shrinking growth.

Greece’s accession to the Eurozone was followed by a largely ignored, rapid, and unsustainable build-up in private sector debt. Once the Greek government was forced to impose severe austerity measures and the economy collapsed, the private debt crisis followed. Now, the large ratio of delinquent loans held by Greek banks is adding to the factors hampering economic growth. For Greece to recover, its private debt problems need to urgently be addressed with an approach that offers relief to both borrowers and lender.

This article will highlight how the mismanagement of the Greek sovereign debt problems triggered the current private debt crisis. We show the rapid growth in private debt, document the macroeconomic context that pushed to Greece into a depression, and explain how these factors created a private debt crisis. Then, we discuss some of the existing proposals for addressing a large number of loan delinquencies and their limitations, and finally, propose other approaches to tackle this pressing problem. This focus on the health of Greek’s non-bank, private borrowers presents us with a different perspective on the infamous “doom loop” between sovereign debt prices and financial balance sheets. The standard “doom loop” interpretation holds that as banks hold sovereign debt, distress in these assets erodes the banks’ capital and leads to a liquidity shock which, in turn, causes a collapse in lending from the banking sector. A fall in investment leads to a contraction in economic activity which, therefore, leads to a more distress for the debt of the sovereign. Conversely, if the sovereign prioritizes growth and “bails out” the banking sector through direct infusions, the state’s spending increases the outstanding stock of debt further thereby lowering its price and hurting the banks’ balance sheets. Focusing on the burdens and performance of the non-bank, non-financial private sector can help us break out of this loop by providing direct support to growth-generating spending.[2]

Private debt build-up in Greece

When Greece joined the Eurozone in 2001, it brought an economic boom. At first, it seemed like Greece was converging with other wealthier Eurozone members. Between 2001 and 2003, Greece enjoyed a real GDP growth of over 4 percent a year.[3] In the early 2000s, as the Greek economy was growing, as were living standards. Average wages, in their dollar equivalent, grew from about $26,000 per year in 2001, to over $30,000 by 2004.[4]

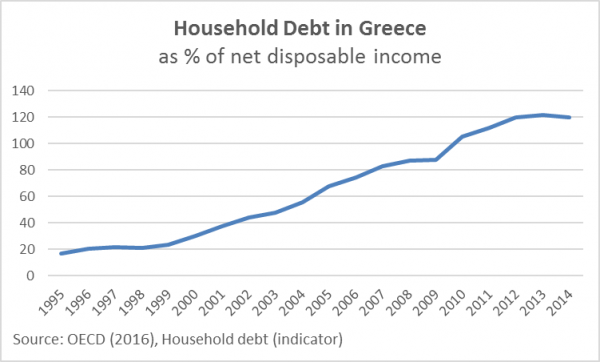

Among the benefits of joining the Eurozone was easier access to credit, both for the public and private sectors in Greece. Being part of the same currency union meant that more money from banks at the center (Germany, France) was flowing into less wealthy periphery countries such as Greece. With easier access to funds, and with interest rates falling, Greek banks expanded their lending causing a small boom in the country’s private sector. A combination of easier access to credit and expectations of future cash flows led to an expansion in household borrowing as illustrated in figure 1.

Figure 1

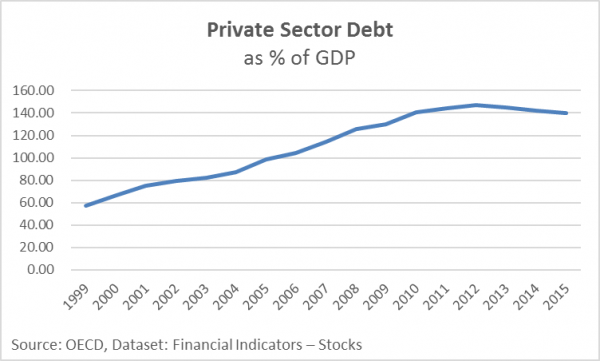

Figure 2

Private sector debt more than doubled as a percentage of GDP. Figure 2 shows that the level of Greek private debt was below 60 percent of GDP in 1999, before it climbing to almost 150 percent of GDP in 2012. Policymakers paid little attention to the growth of private sector debt, or its sustainability.

Greek sovereign debt crisis

As a member of the Eurozone, the Greek government could issue bonds at very low interest rates. Even though the European Central Bank (ECB), through Article 125 of the Lisbon Treaty[5] had a clear “no bailout clause” on sovereign debt, stating that no European Union (EU) country can assume the debt of another EU member, markets assessed similar risks for all Euro-denominated bonds. Without proof of real-side economic convergence, interest rates on bonds from Eurozone members converged in the early 2000s.

Under these assumptions, Greece could borrow at rates almost as low as those of the German government enjoyed, despite the clear differences between the strength of the two economies. The reduction in interest rates and easy access to credit in the early 2000s allowed Greece to increase its sovereign borrowing without much attention. Furthermore, prior to the crisis, to mask excessive debt and comply with EU limits on deficits, the Greek government actively collaborated with its private market makers to mask the true extent of the government deficit.[6] Thus, for a long time, the extent of indebtedness of the Greek government was unknown to markets which assessed its risks on an EU-wide rather than a national basis despite the clear lack of a fiscal union.

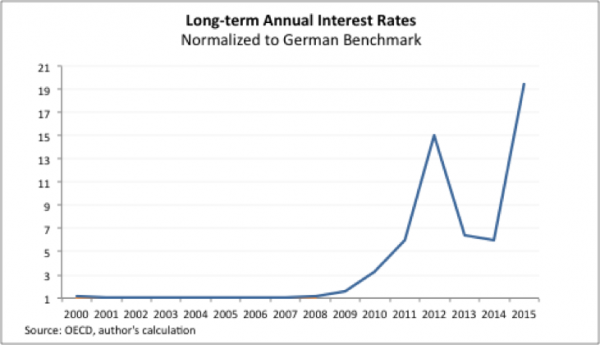

Figure 3

Figure 3 illustrates long-term annual interest rates on Greek government bonds compared to the interest rates on German issued bonds. Greek interest rates moved very close to German rates until 2009. The rates on bonds issued by the two countries started to diverge significantly once it became clear that the Greek government was in severe financial trouble. By 2010, rates for Greece were triple those for Germany, and at the peaks of the later crises they reached levels 15, and 19 times higher, respectively.

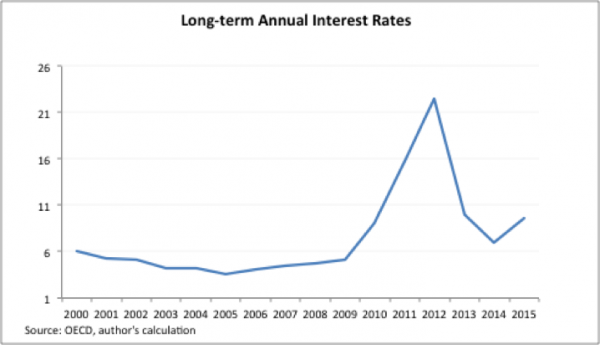

Figure 4

In figure 4, we can see the actual annual interest rates on Greek issued bonds, which exploded after 2008. This development is not surprising, given that EU institutions initially declared they would not help the Greek government with any funds. Thus, to finance its operations, and meet payments on previous debt, the Greek government was forced to keep borrowing on markets at exorbitant costs.

Despite the steep interest rates, Greece needed funds to operate, so it continued borrowing, mostly from banks within the European Union, with French and German banks having particularly high exposure to Greek bonds.[7] The banks that continued lending funds to Greece were aware of the high risk of a default at that point, which is how they justified charging high-interest rates. While the process of obtaining funds at such high costs was clearly unsustainable, it continued until 2010, when Greece officially declared it could no longer pay its bills.

In 2010, EU officials became alarmed with Greece’s high debt-to-GDP ratio. Despite this, we will show it wasn’t until after 2010, when an official bail-out program was imposed on Greece, that the Greek domestic, private economy began to collapse. It was not a too high debt-to-GDP ratio per se that caused the economic meltdown but the response of European monetary authorities that caused Greece to be cut off from external financing which brought the government to the brink of bankruptcy. In the aftermath of the imposed spending cuts, the debt-to-GDP ratio exploded as revenues for the government crumpled and GDP shrunk.

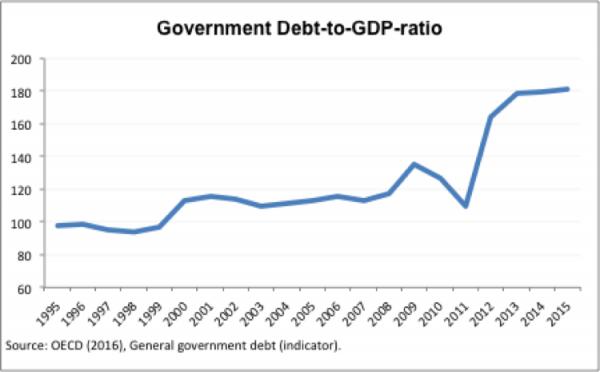

Figure 5

Figure 5 depicts the government debt-to-GDP ratio in Greece between 1995 and 2015. The ratio started to grow after 2008 when it reached about 135 percent of GDP. It fell to 109 percent in 2011, only to explode to 164 percent of GDP in 2012, and has continued to increase since.

How the Greek government accepted a toxic bailout deal

Once Greece could no longer afford to borrow funds on the market, it had little choice but to seek help from EU institutions. At that point, the Greek government had limited choices. As a member of the Eurozone, the Greek government did not have the power to issue currency. Thus, its options were to default on its debt and leave the Eurozone, or accept a bailout from the troika. In 2010, the idea of leaving the Eurozone, with the uncertainty it brought, was extremely unpopular. People feared that the return to a Greek Drachma would result in a severe recession. Thus, the Greek government entered negotiations for a bailout with very little leverage.

In matters of deciding the EU response to the Greek plea for help, Germany, as the strongest European economy, had a larger say, and vehemently opposed any type of debt relief. However, at the point of these negotiations, Greece’s main creditors were European banks, with German banks also heavily exposed to Greek bonds.[8] Allowing Greece to default on its debt meant that those banks would have taken significant losses.

Given these circumstances, the troika of the European Commission, the European Central Bank, and the International Monetary Fund designed a bailout plan for Greece, providing it with the funds for the government to fully repay its private sector, creditors. The bailout agreement explicitly denied Greece the right to attempt to force creditors to restructure its debt, saving them from incurring any losses. This ultimately meant that the troika bailed out other European banks, at the expense of the Greek government.

It is very important to note that the first bailout Greece received went almost entirely to repaying banks holding Greek bonds, many based in France and Germany, for the loans they made to a struggling Greek government at extremely high interest rates. Even though many of the loans were speculative and made after Greek economic troubles were obvious, most of these banks were repaid in full, earning significant profits. The lack of a European safe asset, or a common fiscal instrument that could serve as collateral meant that while banking sector lenders retained their profits, and thus solvency the brunt of the cost was born by the Greek budget alone, therefore not only exacerbating the “doom loop” but localizing its effect on one sovereign that was already suffering a contraction of credit.[9]

In its first bailout assessment in 2010,[10] the EC concluded that the growth in Greece between 2000 and 2009 was the result of unsustainable borrowing of the government, and wages in Greece had grown too fast. The report blames the Greek government for crowding out private investment and structural problems for the economic woes of the country.

The main goal of the first assistance package was to “reassure markets on the determination of the authorities to do whatever it takes to secure medium- and long term fiscal sustainability.”[11] In practice this meant repaying its creditors while cutting public spending to reduce future expenses. The measures centered on ways to cut expenses, by cutting pensions, public sector salaries, and spending on things such as education and healthcare. Meanwhile, through a crackdown on corruption and tax evasion more revenue would be raised. Deregulation of markets would then create a favorable business environment and Greece would recover and repay its debt.

The official assessment was that “real GDP growth is set to contract significantly in 2010–2011 and to recover only slowly thereafter” and claimed the “rebound will only be possible when market and private sector confidence returns and the effects of structural reforms start to materialize.” [12] However, the plan failed and in 2012 additional assistance was required. Rather than changing their approach, the troika just pushed for harsher measures, claiming that Greece simply did not implement sufficient reforms. The second agreement included “a package of measures aimed at reducing Greece’s debt to 124% of GDP by 2020.”[13]

After the second agreement did not lead to the desired results, Greece had to request further support in 2015. The request was approved, with more conditions for the Greek government. Similarly, to the first two agreements that failed to bring the country back on track, the third one included “measures intended to enable the Greek economy to return to a sustainable growth path based on sound public finances, enhanced competitiveness, high employment and financial stability.”[14]

From recession to depression

At the heart of the Troika’s assumptions is a categorical error conflating government fiscal deficit with crowd out and administrative bloat. While government spending can lead to “crowd out” fiscal deficits also can act to “validate” private assets in a period of falling private investment. If we accept the basic axiom that every asset requires a liability, then in the absence of private investment, state budgets must be used to issue liabilities to forestall the collapse of the value of assets. This means that government spending is not directly tied to the size of the state but can actively work with private sector to prevent, or fight an episode of debt deflation.

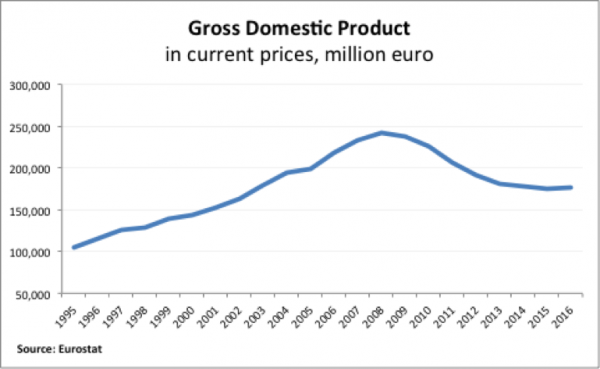

The conflation between budget and competitiveness helps explain why the Troika bailout program only exacerbated the crisis and turned what was a contained sovereign debt crisis into a larger “debt deflation” economic collapse.[15] Despite it being clear that the government had problems financing its spending since 2008, the initial impact on the overall economy was somewhat contained. It was only in the aftermath of the bailouts and austerity measures that the Greek economy effectively entered a depression.

The EC states their programs are designed to “sustain the Greek government’s efforts to address economic imbalances, tackle social challenges, and pave the way for sustainable economic growth and job creation.[16]” In practice, we show the results have been quite the opposite. Greece is still in a deep depression, without any prosperity in sight. While the troika did expect a recession to result from implementing their policies but they assumed recovery would follow within 1 or 2 years. When matters worsened, rather than reassessing their stance, the troika claimed even harsher austerity was needed, and desperately tried to find more “structural issues” to assign the blame for the worsening economic situation. As a result, Greece entered a depression that it has not recovered from to this day. The results are clearly illustrated in figure 6.

Figure 6

Figure 7

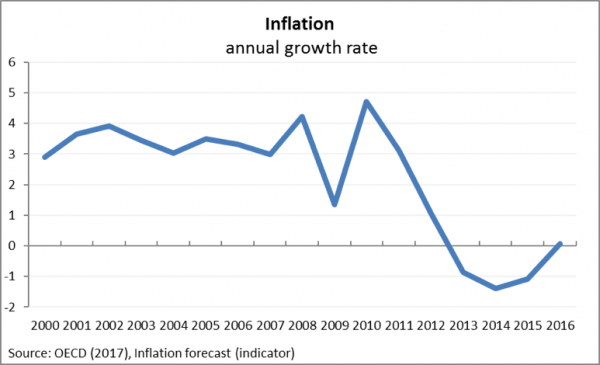

Inflation, as depicted in figure 7, was high amongst EU members, at 3-4 percent, until the crisis. In 2009, there was a drop in inflation, then in 2010, when the government debt debacle had already started, inflation surpassed 4 percent. However, after that inflation decreased, and in 2013, 2014, and 2015 was negative, while in 2016 it was almost 0.

Figure 8

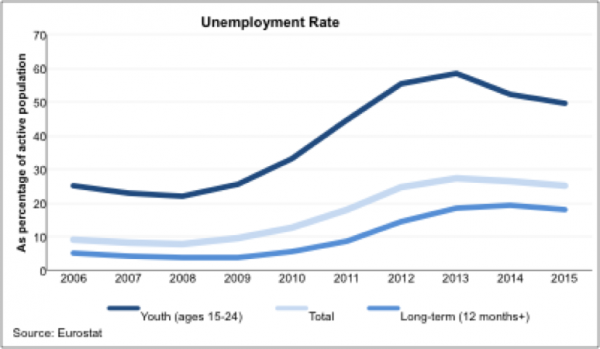

Figure 8 shows total, youth, and long-term unemployment levels in Greece. These indicators started to slowly worsen after 2008. However, it was only after 2010 that they dramatically increased, with little improvement since. Youth unemployment in Greece has reached alarming levels of over 50 percent; long-term unemployment is at almost 20 percent and overall unemployment above 25 percent. While the unemployment rate is no longer growing, there are also no significant improvements towards the reduction of these unemployment levels.

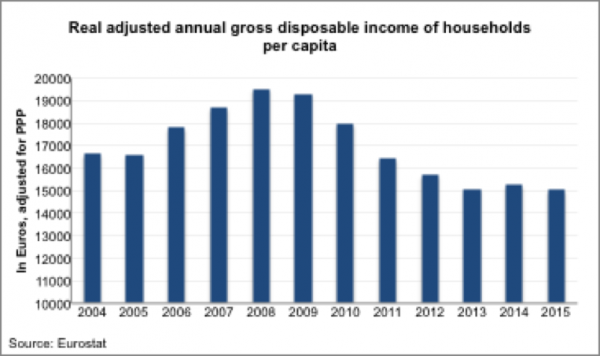

Figure 9

As seen in figure 9, real disposable income registered a small drop of 1 percent compared to the previous year in 2009 and then a sharp drop of almost 7 percent in 2010. Real disposable income fell below 2004 levels in 2011, erasing all gains for Greek households. Ever since real income growth has not returned to Greek people. Overall, between 2008 and 2015, real annual disposable per capita income fell by 23 percent. From 2010 to 2015, it fell by 16 percent.

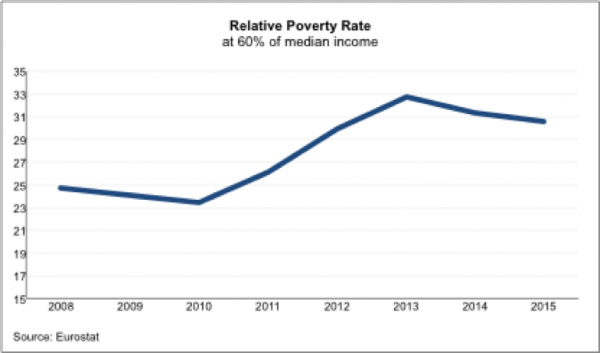

The increase in relative poverty helps paint a clearer picture of eroding living standards in Greece. Despite the overall drop in incomes, relative poverty, which is calculated at a threshold of 60 percent of the median income, increased from about 23 percent in 2010 to almost 33 percent in 2013. It then dropped slightly and was measured at almost 31 percent in 2015.[17]

Figure 10

Figure 10 illustrates the relative poverty rate in Greece between 2008 and 2015. From 2008 until 2010 the poverty gap was slowly closing. However, since 2010 it widened significantly, increasing by 30 percent from 2010 to 2015. Given that this is calculated as a percentage of median income, which as we have seen in figure 9 fell significantly in this time frame, it becomes clear that certain households were more severely impacted by this downturn.

The large decline in GDP can be mostly attributed to the collapse of both consumption and investment.

Figure 11

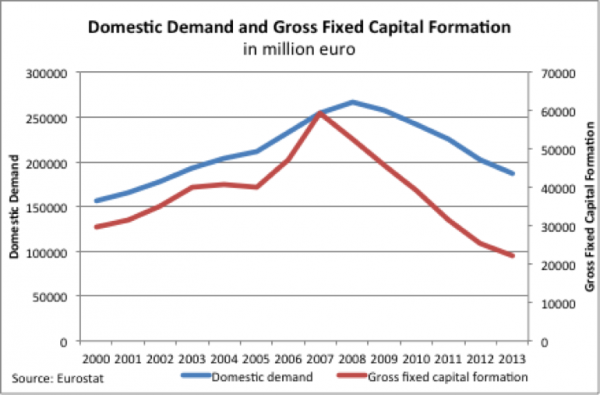

Domestic demand and gross fixed capital formation (GFIC), which measure consumption and investment respectively, are depicted in figure 11. The left axis shows the level of domestic demand, and the right axis the level of GFIC. They both follow similar patterns: they increase in the early 2000s, and then fall. In the case of GFIC, it dropped over 60 percent between 2007 and 2013. Furthermore, the level of GFIC was over 25 percent lower in 2013 than it was in 2000. Domestic demand started falling after 2008 and between 2008 and 2013 it decreased by 30 percent.

Looking at the data, it is clear the bailouts received by Greece did not revive the economy. Rather, they were linked to measures that contributed to mass unemployment, lower incomes, and a drop in GDP that actually facilitated the increase of the debt-to-GDP ratio. The inevitable drop in demand following a depression also contributes to making Greece a less attractive to investors. Both Greek consumers and businesses struggled, and the economy failed to recover. The Greek economy entered a downward spiral in which imposed spending cuts reduce incomes and demand, further contract the economy, and limit its ability to repay its debts. The question that remains is what caused these dramatic results? In the next section I will argue that because of the terms of its bailouts, the Greek private sector was hit with a double punch of a collapse in private investment and a cutback in state issued investment. Households and businesses which expected future cash flows to repay their debts suddenly found themselves illiquid, thereby devastating the Greek economy.

The private debt crisis

Since 2000, private sector debt has doubled as a percentage of GDP, while real incomes are the same level. While the ratio of private sector debt-to-GDP, at about 120% (figure 2), is not alarming in it of itself, its rapid growth along with stagnating incomes, negative or very low inflation, and a collapsing economy make it a major issue driving Greece’s inability to grow out of its depression.

The start of the rapid increase in private sector debt coincided with a period of strong economic growth for Greece. However, after economic growth slowed down, private sector debt continued to grow at a very fast pace — something that should have been a reason for concern long before Greece’s sovereign debt problems came to light. However, this speculative borrowing was still sustainable, given expectations of continuing economic growth providing private borrowers with returns on their investments.

Spurred by this increased optimism and the easy access to credit, private debt as a share of disposable income exploded. In 2000, private debt was about 30 percent of disposable income. While income was growing fast in the early 2000s, private debt grew much faster. By 2008, private debt has reached a level of 87 percent of income, which would have been worrisome even under a favorable macroeconomic context.

When the failures of European authorities, the IMF, and the ECB to properly respond to Greece’s sovereign debt problems pushed the economy into a depression, this in turn also triggered a major private sector debt crisis. Initially, the private sector continued to borrow more, and private debt increased to over 120 percent of disposable income by 2012. As the economic downturn worsened, private entities started to struggle with repaying their own debts.

Evidence of this is seen in the increase of non-performing loans (NPLs) on the balance sheets of Greek banks. The IMF defines loans as “non-performing” when payments are past due by 90 days, or there are other reasons, such as the borrower filing for bankruptcy, to assume the loan would not be repaid in full.[18] The loans maintain this qualification until some payment on them is made, or they are written off.

Usually, the total NPLs in an economy are less than 2 percent of all loans outstanding, which makes it easier for banks to simply write them off with little damage to their balance sheet positions. Under normal circumstances, the failure to repay a loan is placed on individual borrowers. Banks consider the risk of some borrowers defaulting and include this risk in the calculation of the interest rates they charge to have room to write off a small amount of NPLs as losses. However, in a “debt-deflation” scenario as we are experiencing in Greece, NPLs became a systemic problem. Given the very unfavorable macroeconomic circumstances, individual borrowers can no longer be blamed for their inability to make payments on their debts while Greek banks face such overwhelming pressure on their balance sheets that they are unable to write off their losses while remaining solvent. Instead of the majority of cash flows generated by private activity going to consumption or reinvestment, therefore spurring economic growth, it goes to attempting to repay debts. Financial institutions, on the other hand, stop making new loans at reasonable rates to entrepreneurs due to their weak balance sheet positions.

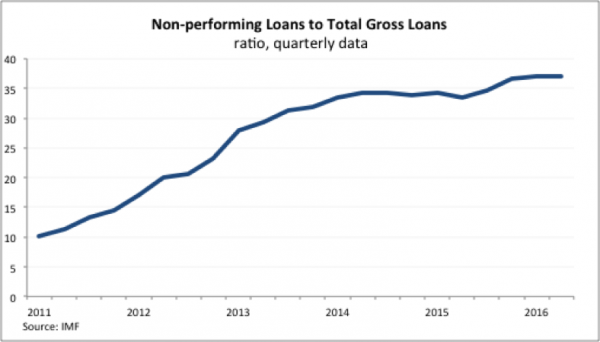

In its 2010 evaluation of Greece, the EC first expressed concern over the increase of NPLs in the Greek banking system.[19] The commission thought that an increase in NPLs from 5 percent in 2008 to 7.7 percent in 2009 was worrisome. By the second quarter of 2016, that number had jumped up to 37 percent.

Figure 12

Figure 12 illustrates the quarterly data regarding NPLs in Greece made available by the IMF. From the 5 percent number cited by the EC for 2008, the NPL ratio reached 37 percent. Between 2011 and 2012, the NPL ratio increased from 12 to 20 percent and then grew to 30 percent in 2013. The growth in the NPL ratio has somewhat slowed down but it is still on a steadily upwards path.

The timing of the explosion in loan defaults perfectly coincides with the start of the depression and the sharp decline in income and demand. As a report[20] by the Hellenic Observatory at LSE points out, “when economic activity slows down, NPLs increase as unemployment rises, disposable incomes decline and borrowers face difficulties in repaying their debt obligation.” The report concludes that the “sharp increase in non-performing loans can be mainly attributed to the unprecedented contraction of domestic economic activity.”

This link is also clearly stated in a 2000 IMF study[21] of NPLs, which finds that “the amounts involved in nonperforming loans may rise considerably as a result of less predictable incidents.” As an example of what these incidents might look like, the study suggests events that are on a much smaller scale than an entire economy collapsing, such as for example one major company failing. In that case, the problem is systemic and blame for default can no longer be assigned to individual borrowers. The macroeconomics analysis group Euromonitor also linked rising NPLs to “sliced disposable incomes, booming unemployment rates, rising taxation and general uncertainty,” naming them “one of the hottest issues of the political agenda.”[22]

Perhaps most important is the February 2017 EC’s quarterly report[23] on the Euro area, which dedicated an entire volume to the issue of NPLs. In the report, the commission admits there is a clear causality between recessions and an increase in NPLs: “During recessions and periods of weak economic growth, corporates and households are more likely to fall behind with the repayment of their loans.”

The macroeconomic challenges that resulted in the aftermath of the economic crisis definitely played a central role in exacerbating the NPL crisis in Greece. However, it is essential to also acknowledge the part played by a highly indebted private sector that was accumulating liabilities at an unsustainable pace prior to the sovereign debt problems. This overextended private sector was particularly susceptible to a private debt crisis.

The troika’s take on NPLs

The consensus amongst European institutions seems to be that NPLs hamper and hold back economic growth through damage inflicted on the banking system that is causing a reduction in the available credit supply. Given the general supply-side, free market policies proposed by these institutions, this approach is to be expected. The EU has been vehement on protecting banks, clearly requesting in one of the bailout agreements[24] that “all necessary policy actions will be taken to safeguard financial stability and strengthen the viability of the banking system.” However, the creditors have not offered any answer to the demand side damage inflicted by the contraction of Greek spending due to systemic failures in loan repayments.

In a report issued by European Parliament, the main conclusion is “that higher NPLs tend to reduce the credit-to-GDP ratio and GDP growth while increasing unemployment.” [25] The EC[26] expresses fear with the possibility of “a vicious cycle of low asset quality, low bank profitability, rising capital requirements and constrained lending.” The European Banking Authority[27] (EBA) is also concerned with capital being tied up in NPLs and lower profitability for banks.

Until now the troika’s concern for the health of the banking system ensured that Greek banks gained access to bailout funds and stayed afloat. From the total of 230 billion euros in bailout funds, almost 50 went towards recapitalizing Greek banks.[28] However, Euromonitor[29] paints a bleak picture of the Greek banking system. Despite banks benefiting from recapitalizations, consumer lending, an important factor in generating economic activity, is at a “historic low.” They predict that even if banks have access to liquidity, they would still prioritize more profitable business over consumer credit.

The latest agreement between Greece and its creditors[30] is demanding the Greek government “immediately take steps to tackle NPLs.” However, relief for borrowers is not exactly what the EC has in in mind. One of the requirements is to no longer defer payments on loans for mortgages of primary residences, and move on to repossessions of homes. The EC suggests moving forward with creating a secondary market for NPLs, which means those purchasing the debt will move forwards aggressively to collect as much as possible from borrowers, with the help of a legal framework that Greece ought to introduce. This will not help, but only worsen, the collapse in household finances and only drive Greece toward further economic distress.

The EU demanded, “the creation of out-of-court procedures and the acceleration of judicial procedures, by reducing the timeline for debt restructuring, also improve the value of NPL and reduce creditors’ losses.”[31] Later, it demanded Greece introduce legislation that would liberalize the sale of NPLs on secondary markets. The explicit plan of the EC is the “development of a dynamic NPL market,”[32] which falls into the same category of reforms that seek business-friendly deregulation at the expense of average people.

These conditions solely focus on improving the balance sheets of banks and disregard those of the borrowers that can no longer afford to repay their loans. The plan put forward by the troika relieves pressure from banks, not from borrowers, and further feeds into the vicious cycle of low demand that is stalling the recovery. Repairing bank balance sheets without restoring consumer demand would just mean that credit has nowhere to go—in effect the Troika encourages Greeks to “push on a string.” To truly solve the problem of NPLs, relief needs to be extended to both lenders and borrowers.

The way forward

The Greek private debt crisis and the resulting high ratio of NPLs is a consequence of the depression. It is important the troika assumes responsibility for their mistakes and helps Greece. There is no doubt that NPLs are a huge burden on Greek banks. However, allowing them to unload the debt, without offering appropriate relief to the borrowers, will likely not have the desired impact on credit growth given the overall circumstances in the Greek economy. Indeed, Greece’s NPL crisis should foster a larger conversation about the European monetary system and the place of private borrowers in it.

Cleaning up the balance sheets of Greek banks won’t jumpstart the economy. Restructuring both the Greek public and private debt, and allowing for some stimulus would have a larger positive impact on the economy if both the public and private sector were in a position to spend money and create demand in the economy. Moreover, the creation of a European-wide safe asset or transregional fiscal response to private debt buildups would open space to give distressed bank lenders liquidity without directly bailing them out, while offering the possibility of fostering demand-led growth.

While Greece continues to be punished by European authorities, all other Eurozone members have gained access to quantitative easing from the ECB. Under a new asset purchase program, the ECB is providing liquidity to institutions in other member states.[33] Greece was excluded from this program on the premise that its bonds are not high-quality assets. However, for bonds that are purchased to solely sit on the balance sheet of the ECB, this seems like a rather weak reason.

If the ECB truly wanted to help Greece recover and aid the banking system it could provide the liquidity it needs directly to it, or purchase its NPLs directly (similarly to how the Federal Reserve bought worthless mortgage-backed securities in the aftermath of the Great Recession). Furthermore, if the ECB purchased NPLs, by not aggressively seeking loan collection, it would also offer relief to borrowers.

Despite constantly citing market forces in all its prescriptions for Greece, the troika provided the funds to the Greek government to repay its Western European creditors and the ECB is currently acting as a lender of last resort for all Eurozone members except Greece. Clearly, market forces are not important when they put big banks in Western European countries at risk.

[1] http://www.bankofgreece.gr/BoGDocuments/20160310_The_Agenda_for_NPL_Resolution.pdf

[2] Emauel Farhi and Jean Tirole “Deadly Embrace: Sovereign and Financial Balance Sheet Doom Loops” NBER Working Paper no. 21843 (January, 2016).

[3] OCCD (2016), Gross domestic product (indicator).

[4] OECD (2016), Average wages (indicator).

[5] http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:12012E/TXT

[6] http://www.nytimes.com/2010/02/14/business/global/14debt.html?pagewanted=all

[7] http://www.newyorker.com/news/john-cassidy/greeces-debt-burden-the-truth-finally-emerges

[8] http://www.nytimes.com/2010/04/29/business/global/29banks.html

[9] https://www.theatlantic.com/business/archive/2015/07/greece-crisis-banks-greedy/398603/; On European-safe assets and the doom loop see Markus K. Brunnermeier et al., “ESBies: Safety in the Tranches,” Economic Policy 32, no. 90 (April 1, 2017): 175–219, doi:10.1093/epolic/eix004.

[10] http://ec.europa.eu/economy_finance/publications/occasional_paper/2010/pdf/ocp61_en.pdf

[11] http://ec.europa.eu/economy_finance/publications/occasional_paper/2010/pdf/ocp61_en.pdf

[12] http://ec.europa.eu/economy_finance/publications/occasional_paper/2010/pdf/ocp61_en.pdf

[13] http://ec.europa.eu/economy_finance/assistance_eu_ms/greek_loan_facility/index_en.htm

[14] http://ec.europa.eu/economy_finance/assistance_eu_ms/greek_loan_facility/index_en.htm

[15] Steve Keen, “Finance and Economic Breakdown: Modeling Minsky’s ‘Financial Instability Hypothesis,’” Journal of Post Keynesian Economics 17, no. 4 (1995): 607–35.

[16] http://ec.europa.eu/economy_finance/assistance_eu_ms/greek_loan_facility/index_en.htm

[17] Relative poverty gap (cut-off point: 60% of median equivalised income)

[18] https://www.imf.org/external/pubs/ft/bop/2005/05-29.pdf

[19] http://ec.europa.eu/economy_finance/publications/occasional_paper/2010/pdf/ocp61_en.pdf

[20] http://www.lse.ac.uk/europeanInstitute/research/hellenicObservatory/CMS%20pdf/Publications/GreeSE/GreeSE%20No.101.pdf

[21] https://www.imf.org/external/pubs/ft/wp/2001/wp01209.pdf

[22] http://www.euromonitor.com/consumer-lending-in-greece/report

[23] https://ec.europa.eu/info/publications/economy-finance/quarterly-report-euro-area-qrea-vol-16-no-1-2017_en

[24] http://ec.europa.eu/economy_finance/assistance_eu_ms/greek_loan_facility/pdf/01_mou_20150811_en.pdf

[25] http://www.europarl.europa.eu/RegData/etudes/BRIE/2016/574400/IPOL_BRI(2016)574400_EN.pdf

[26] https://ec.europa.eu/info/publications/economy-finance/quarterly-report-euro-area-qrea-vol-16-no-1-2017_en

[27] https://www.eba.europa.eu/documents/10180/1360107/EBA+Report+on+NPLs.pdf

[28] http://www.nytimes.com/2015/07/31/business/bailout-money-goes-to-greece-only-to-flow-out-again.html

[29] http://www.euromonitor.com/consumer-lending-in-greece/report

[30] http://ec.europa.eu/economy_finance/assistance_eu_ms/greek_loan_facility/pdf/01_mou_20150811_en.pdf

[31] http://www.europarl.europa.eu/RegData/etudes/BRIE/2016/574400/IPOL_BRI(2016)574400_EN.pdf

[32] http://ec.europa.eu/economy_finance/assistance_eu_ms/greek_loan_facility/pdf/01_mou_20150811_en.pdf

[33] https://www.ecb.europa.eu/mopo/implement/omt/html/index.en.html